Division C – Emergency Family and Medical Leave Expansion Act

- Employers covered: It covers employers with fewer than 500 employees, including small employers who are not covered by the FMLA.

- To be eligible for the new leave, an employee need only have been employed for 30 days. There is no minimum requirement for hours worked, so part-time employees are eligible as well.

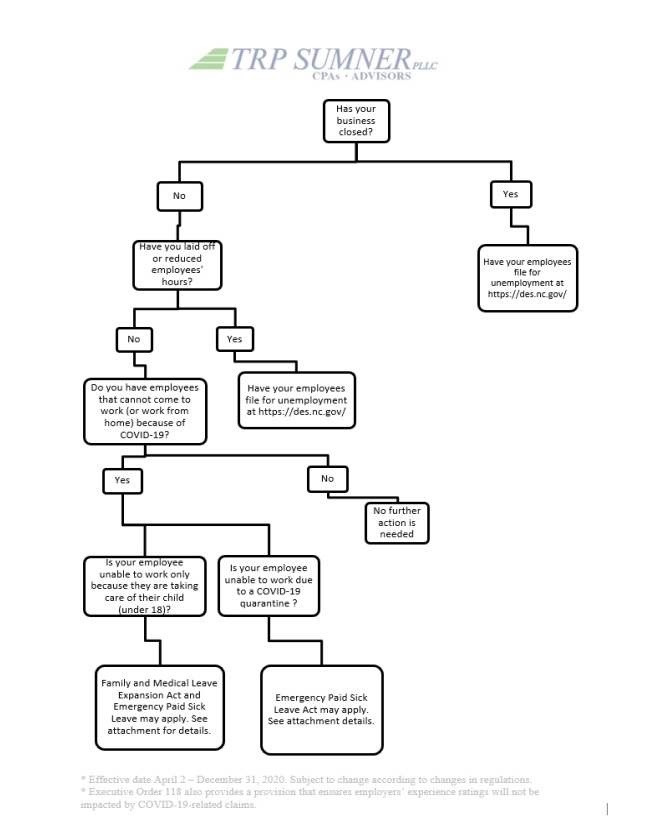

- The FMLA Expansion Act provides that an eligible employee must be allowed protected leave if the employee is unable to work (or work from home) in order to care for a son or daughter under the age of 18 whose school has been closed, or whose regular childcare provider is unavailable due to a public health emergency.

- Amount of paid and unpaid leave: The FMLA Expansion Act provides as follows:

- An eligible employee is allowed 12 weeks of FMLA leave.

- The first 10 days may be unpaid (see discussion of the Paid Sick Leave Act). An employee may elect to substitute accrued paid leave during this 10-day period However, an employer may not require the employee to use such paid leave.

- Paid leave must be provided for each day of leave after the first 10 days of leave and is subject to a cap of $200 per day or $10,000 in total.

- Subject to the caps, pay for leave is calculated based on two-thirds of the employee’s regular rate of pay (or minimum wage, whichever is greater), for the number of hours the employee would otherwise be normally scheduled to work.

- Please refer to the publication to find more information about pay calculation for part-time employees.

- Department of Labor potential exemptions: The FMLA Expansion Act gives the Secretary of Labor authority to issue regulations for good cause to: (i) exclude healthcare providers and emergency responders from eligibility, and (ii) exempt small businesses with fewer than 50 employees from coverage if the imposition of such requirements would cause financial hardship to the business. Please contact the Department of Labor to determine if you meet the criteria for an exemption.

- The FMLA Expansion Act will be effective no later than April 2, 2020 and will sunset on December 31, 2020.

Division E – Emergency Paid Sick Leave Act

The provisions under the Emergency Paid Sick Leave Act (“Paid Sick Leave Act”) portion of the COVID-19 Response Act imposes new requirements on employers to provide two weeks of sick pay, in addition to employer’s existing sick pay or sick leave policies, filling the gap left by the paid leave provisions of the portion of the bill discussed above under the FMLA Expansion Act.

- Employers covered: Any employer with fewer than 500 employees.

- Eligible employees: Any employee, with no minimum period of employment, is eligible.

- Reasons for allowed sick pay:

- The employee is subject to a federal, state, or local quarantine or isolation order related to COVI-19.

- The employee has been advised by a health care provider to self-quarantine.

- The employee has symptoms of COVID-19 and is seeking a medical diagnosis.

- The employee is caring for an individual subject to a government quarantine or isolation order or had been advised by a healthcare provider to self-quarantine.

- The employee is caring for his or her child if the child’s school or place of care has been closed, or the child’s care provider is unavailable due to COVID-19 precautions.

- The employee is experiencing any other substantially similar condition specified by the Secretary of Health and Human Services in consultation with the Secretary of the Treasury and the Secretary of Labor.

- Amount of hours of paid sick time:

- For full-time employees: 80 hours.

- For part-time employees: the equivalent of two weeks’ worth of regular hours .

- Paid sick time may not be carried over from year to year.

- Amount of pay:

- For employees taking paid sick leave to fulfill caregiving obligations to family members: Two-thirds of the employee’s regular rate of pay (or minimum wage, whichever is greater), subject to a limit of $511 per day or $5,110 in total.

- For employees taking paid sick leave due to their own quarantine or isolation, diagnosis, or symptoms: The greater of the employee’s regular wages and the applicable federal, state, or local minimum wage, subject to a limit of $200 per day or $2,000 in total.

- Please refer to the publication to find more information about pay calculation for part-time employees.

- Department of Labor potential exemptions: The Secretary of Labor is authorized to issue regulations for good cause to: (i) exclude healthcare providers and emergency responders from eligibility; and (ii) exempt small businesses with fewer than 50 employees from coverage if the imposition of such requirements would cause financial hardship to the business. Please contact the Department of Labor to determine if you meet the criteria for an exemption.

- Additional requirements:

- Employers are prohibited from requiring employees to find replacement coverage as a condition for using paid sick leave.

- Employers may not take adverse employment action or retaliate against employees who take paid sick leave pursuant to the Paid Sick Leave Act.

- Paid sick leave under the Paid Sick Leave Act is in addition to an employer’s existing sick pay or sick leave policies, and employers may not change such policies after the date of enactment to avoid the new requirements.

- Employers may not require employees to use paid sick leave under an employer policy before using sick leave under the Paid Sick Leave Act.

- Employers are required to post notices prepared by the secretary of Labor that informs employees of their rights to paid sick leave pursuant to the Paid Sick Leave Act.

Tax Credits for Paid Sick Leave and Family and Medical Leave

The COVID-19 Response Act provides a series of refundable tax credits for employers providing paid emergency sick leave of FMLA leave, including tax relief for self-employed individuals.

Sick Leave credit:

For an employee who is unable to work because of Coronavirus quarantine or self-quarantine or has Coronavirus symptoms and is seeking a medical diagnosis, eligible employers may receive a refundable sick leave credit for sick leave at the employee’s regular rate of pay, up to $511 per day and $5,110 in total, up to10 days.

For an employee who is caring for someone with Coronavirus, or is caring for a child because the child’s school or child care facility is closed, or the child care provider is unavailable due to the Coronavirus, eligible employers may claim a credit for two-thirds of the employee’s regular rate of pay, up to $200 per day and $2,000 in total, for up to 10 days.

Child Care Leave Credit (FMLA):

In addition to the sick leave credit, for an employee who is unable to work because of a need to care for a child whose school or child care facility is closed or whose child care provider is unavailable due to the Coronavirus, eligible employers may receive a refundable child care leave credit. This credit is equal to two-thirds of the employee’s regular pay, capped at $200 per day or $10,000 in total. Up to 10 weeks of qualifying leave can be counted towards the child care leave credit. Eligible employers are entitled to an additional tax credit determined based on costs to maintain health insurance coverage for the eligible employee during the leave period.

Prompt Payment for the Cost of Providing Leave

Under guidance that will be released next week, eligible employers who pay qualifying sick or child care leave will be able to retain an amount of the payroll taxes equal to the amount of qualifying sick and child care leave that they paid, rather than deposit them with the IRS.

The payroll taxes that are available for retention include withheld federal income taxes, the employee share of Social Security and Medicare taxes, and the employer share of Social Security and Medicare taxes with respect to all employees.

Examples

If an eligible employer paid $5,000 in sick leave and is otherwise required to deposit $8,000 in payroll taxes, including taxes withheld from all its employees, the employer could use up to $5,000 of the $8,000 of taxes it was going to deposit for making qualified leave payments. The employer would only be required under the law to deposit the remaining $3,000 on its next regular deposit date.

If an eligible employer paid $10,000 in sick leave and was required to deposit $8,000 in taxes, the employer could use the entire $8,000 of taxes in order to make qualified leave payments and file a request for an accelerated credit for the remaining $2,000.

Equivalent child care leave and sick leave credit amounts are available to self-employed individuals under similar circumstances. These credits will be claimed on their income tax return and will reduce estimated tax payments.

For additional information, please visit:

Internal Revenue Service Coronavirus Tax Relief

North Carolina Department of Commerce – Employment Security:

North Carolina Department of Health and Human Services:

Executive Order 118: